In 2Q24, Samsung Maintained Leadership in NAND Flash Market

With 36.9% market share

This is a Press Release edited by StorageNewsletter.com on October 3, 2024 at 2:01 pmThis market report was published on September 20, 2024 by TrendForce Corp.

NAND Flash: Embracing a New Development Phase

In 2024, the storage market is experiencing dynamic changes, with many positive developments, including rising contract prices, significant revenue growth for manufacturers, and multiple breakthroughs in technology. Amid this, major storage companies are gearing up for new challenges, especially as the NAND flash memory sector faces an impending shift.

How Far Have Major Companies Progressed with NAND Flash Technology?

This year, major storage manufacturers like Samsung, Micron, and SK Hynix have all made notable advancements in NAND flash technology.

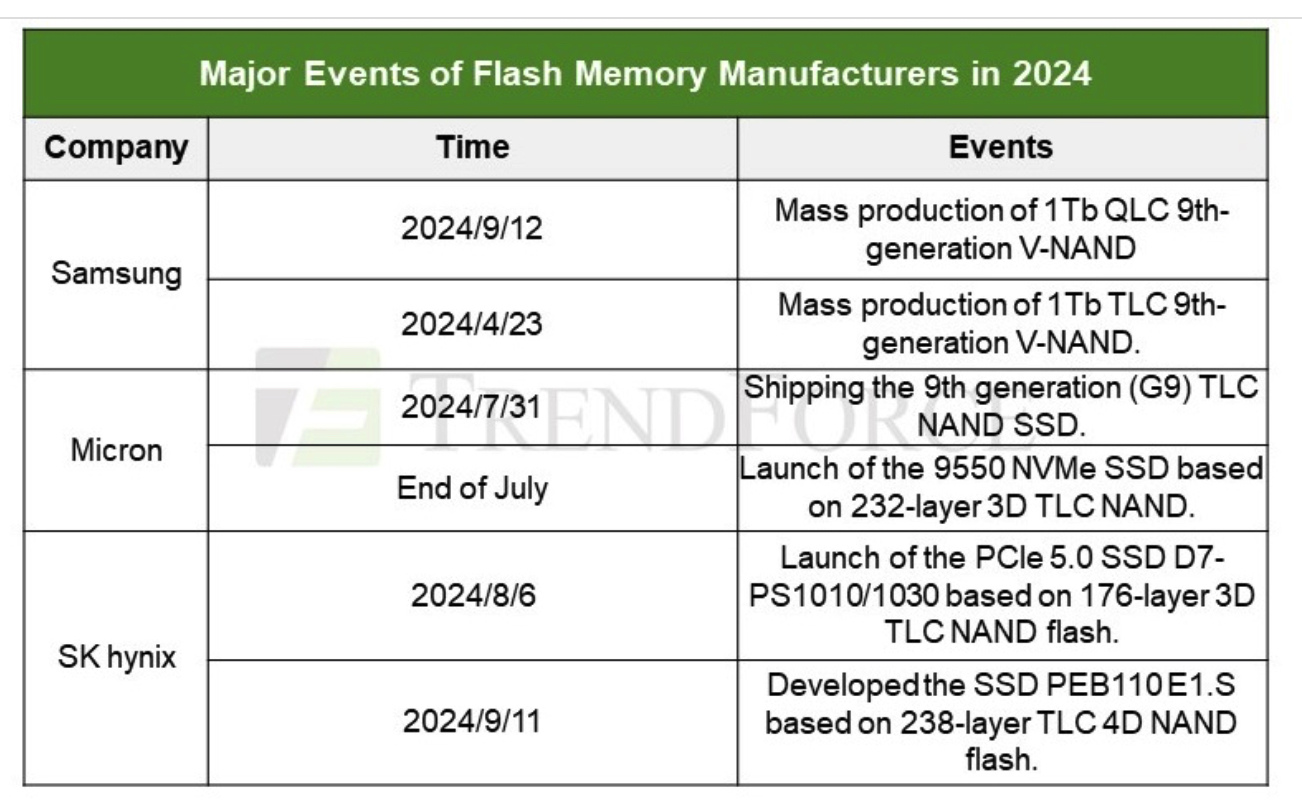

In terms of NAND cell technology, Samsung has become the first in the industry to mass-produce its 9th gen V-NAND with QLC technology. On September 12, it announced it had begun mass production of its 1Tb QLC 9th gen vertical NAND (V-NAND), incorporating several groundbreaking technologies.

From a technological innovation perspective, Samsung’s 9th gen QLC V-NAND employs its unique channel hole etching technology to achieve the industry’s highest stack height with a dual-stack structure. Leveraging the expertise of TLC 9th gen V-NAND, the cell area and peripheral circuits are optimized, resulting in an 86% higher bit density than the previous generation.

Compared to earlier versions, the design of Samsung’s 9th gen QLC V-NAND improves data retention performance by about 20%, enhancing product reliability. Writing performance has doubled, and data input/output speeds have increased by 60%.

Additionally, its low-power design reduces power consumption for both read and write operations by approximately 30% and 50%, respectively. This is achieved by sensing only the necessary bit lines (BL) to minimize power usage.

In terms of applications, Samsung plans to expand the use of the 9th gen QLC V-NAND from branded consumer products to mobile universal flash storage (UFS), PC, and server SSDs to meet the demands of customers, including cloud service providers.

Sung Hoi Hur, EVP and head of flash product and technology at Samsung Electronics, stated that as the enterprise SSD market grows rapidly and demand for AI applications increases, the company will continue to strengthen its leadership in the high-capacity, high-performance NAND flash market through 9th-generation QLC and TLC V-NAND.

However, at present, the mainstream products in the market are still TLC NAND flash memory particles.

On August 6, SK Hynix’s Solidigm launched PCIe 5.0 data center SSDs, the D7-PS1010/1030 series, based on its 176-layer 3D TLC NAND.

On September 11, it announced the development of its high-performance SSD “PEB110 E1.S” for data centers, available in 2TB, 4TB, and 8TB versions. Currently undergoing validation with global data center customers, SK Hynix plans to begin mass production in 2Q25.

On the other hand, Micron announced in late July that its SSD products featuring 9th gen (G9) TLC NAND technology had entered mass production, targeting personal devices, edge servers, enterprises, and cloud data centers. G9 NAND achieves a data transfer rate 50% faster than current NAND technology used in SSDs. Its per-chip write and read bandwidths are 99% and 88% higher, respectively, than other NAND solutions. The Micron 2650 NVMe SSD, based on G9 NAND, achieves near-PCIe 4.0 performance levels, with a sequential read speed of up to 7,000 MB/s.

Micron also launched its new data center SSD, the 9550 NVMe SSD, featuring 232-layer 3D TLC NAND. It supports various AI workloads, offering a sequential read speed of 14.0GB/s and a write speed of 10.0GB/s – 67% higher than competitive SSDs. The 9550 SSD’s random read speed reaches 3,300,000 IO/s, 35% higher than competitors, with random write speeds 33% higher.

The future of QLC SSDs is promising

Industry information indicates that NAND flash, the core medium for storage, is vital for SSD performance. Current SSDs use both TLC and QLC flash.

In the AI era, there is a growing demand for storage, with SSDs playing a critical role. According to TrendForce, SSDs not only store model parameters during AI model training but also create checkpoints to save progress, making them crucial for high-speed data transfer and durability. As a result, customers primarily opt for 4TB/8TB TLC SSDs to meet the rigorous demands of AI training processes.

QLC SSDs, however, are gaining attention due to their higher storage density, which optimizes server space and reduces energy consumption. They can help large-scale data centers lower their TCO while still meeting high-performance storage needs. Industry experts predict that as more data is generated in the form of videos and images, requiring larger storage capacities, TLC/QLC SSDs of 16TB or more will become the primary products for AI inference applications.

According to TrendForce, AI-related SSD procurement is expected to exceed 45EB in 2024, with SSD demand in AI servers projected to grow by over 60% annually in the coming years. The share of AI SSDs within the NAND flash market could rise from 5% in 2024 to 9% in 2025.

The Changing Landscape of the NAND Flash Market

On September 9, TrendForce’s latest research indicates that in 2Q24, Samsung maintained its global leadership in the NAND flash market with a 36.9% market share, up 0.2% from the previous quarter. SK Group followed with a 22.1% share, down 0.1%. Other key players include Kioxia (13.8%), Micron (11.8%), and Western Digital (10.5%).

In terms of revenue, Samsung, SK Group, Kioxia, Micron, and Western Digital all experienced Q/Q growth in NAND flash revenues during the 2Q24. Overall, NAND flash revenue increased by 14% in 2Q24.

TrendForce indicates that as the inventory adjustments for server endpoints near completion and AI drives demand for high-capacity storage products, NAND flash prices continued to rise in 2Q24. However, due to high inventory levels at PC and smartphone manufacturers, NAND flash bit shipments decreased by 1% Q/Q. Despite this, the average selling price increased by 15%, with total revenue reaching $16.796 billion, a 14.2% increase from 1Q24.

Looking ahead to 3Q24, TrendForce expects that all NAND flash suppliers have returned to profitability as of 2Q24 and plan to expand production capacity in 3Q24 to meet strong demand from AI and servers. However, due to weak market performance in the PC and smartphone sectors in 1H24, it is challenging to boost NAND flash shipments. It is estimated that the average selling price of NAND flash products will increase by 5% to 10% in 3Q24, while bit shipments may decrease by at least 5% due to a lack of peak season demand. Industry revenue is expected to remain roughly the same as the previous quarter.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter