Veeco: Fiscal 2Q24 Financial Results

Veeco: Fiscal 2Q24 Financial Results

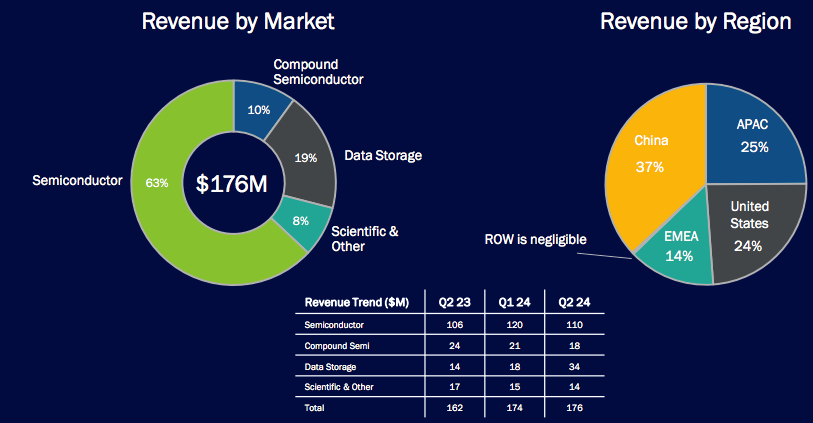

Storage (19% of global revenue) at $34 million up 89% Q/Q and 143% Y/Y, and anticipated to grow 5% to 10% Y/Y

This is a Press Release edited by StorageNewsletter.com on August 14, 2024 at 2:02 pm| (in $ miliion) | 2Q23 | 2Q24 | 6 mo. 23 | 6 mo. 24 |

| Revenue | 161.6 | 175.9 | 315.1 | 350.4 |

| Growth | 9% | 11% | ||

| Net income (loss) | (85.3) | 14.9 | (76.6) | 36.8 |

Veeco Instruments Inc. has reported its second-quarter earnings, aligning with its previously issued guidance. The company announced a revenue of $176 million, non-GAAP operating income of $28 million, and non-GAAP EPS of $0.42.

Semiconductor business showed strength, with record revenues in laser annealing and a positive outlook for the advanced logic and memory segments. The company’s focus on expanding its laser annealing, ion beam deposition, and compound semiconductor businesses was evident, as it emphasized investments in its core technologies and evaluation programs aimed at addressing tier-1 customer challenges.

Key Takeaways

- Veeco’s 2FQ24 results matched guidance with revenues at $176 million and non-GAAP EPS of $0.42.

- Record laser annealing revenue and new orders in advanced logic and memory drove performance.

- The company is investing in laser annealing, ion beam deposition, and compound semiconductors.

- 3FQ24 revenue is projected between $170 million and $190 million, with a tightened 2024 guidance of $690 million to $730 million.

- Veeco sees high single-digit to low double-digit growth in the semiconductor market.

- China is expected to make up about 1/3 of Veeco’s business this year, with strong customer activity.

- Storage sector revenue is anticipated to grow 5% to 10% Y/Y.

Company Outlook

- Veeco plans to expand its evaluation programs in 2025, despite being resource-limited.

- It is cautious about overextension and is narrowing its financial guidance range for the year.

- It anticipates the semiconductor market to grow in high single to low double digits.

- The compound semiconductor space’s contribution is expected to be slightly lower.

- Storage sector revenue is projected to increase by 5% to 10% compared to last year.

- The firm expects 2FQ24 to perform similarly to 3FQ24.

Bearish Highlights

- There has been a decrease in customer deposits, particularly in the storage sector.

- The company’s systems business is expected to be lower in 1FH25 compared to 2024.

- Utilization rates in the storage industry are historically low, reducing service run rate business.

Bullish Highlights

- Veeco has placed 2 ion beam deposition systems and one laser annealing system in the field recently.

- It sees potential growth in ion beam deposition technology for low-resistance metals in the memory market.

- Significant progress has been made in silicon carbide, with plans to place 2 evaluation systems by the end of this year or early 2025.

- The 300-millimeter GaN on silicon evaluation is advancing well, with the tool being turned over to the customer.

Misses

- No specific misses were mentioned in the provided context.

Q&A highlights

- The company discussed the cautious approach of customers in the storage sector towards adding new capacity.

- It provided updates on the progress in silicon carbide and GaN-on-silicon technologies.

- The visibility of opportunities in energy-assisted magnetic recording in storage will become clearer in 2H25.

Comments

Veeco delivered 2FQ24 top and bottom line results in line with guidance. Revenue totaled $176 million (up 9% from 2FQ23 and 1% Q/Q, non-GAAP operating income $28 million and non-GAAP EPS of $0.42.

2FQ24 revenue by market and region

Semiconductor business remains strong highlighted by record laser annealing revenue and new LSA orders in advanced logic and memory. In logic, the company received follow on orders for a leading customers gate all around architecture. And in DRAM, it continues to receive follow-on business to support its customer's planned expansion.

2FQ24 revenue is expected between $170 million and $190 million.

By market, the firm expects growth sequentially in semiconductor and similar levels of revenue for the remaining markets. It expects gross margin between 43% and 44%, Opex between $48 million and $50 million, net income between $24 million and $31 million, and diluted EPS between $0.39 and $0.49 on 63 million shares. And now for some additional color beyond 3FQ24 as the firm is halfway through the year. It is tightening its 2024 revenue guidance to $690 to $730 million from its prior range of $680 to $740 million and correspondingly, it now expects diluted non-GAAP EPS for the full year between $1.65 and $1.85 per share from prior range $1.60 to $1.90 per share.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter