NAND Flash Revenue for 1Q21 Rises by 5% Q/Q

Thanks to better-than-expected demand for notebooks and smartphones, despite shortage of NAND flash controller ICs

This is a Press Release edited by StorageNewsletter.com on June 1, 2021 at 2:31 pm![]() This market report, published on May 26, 2021, was written by Ben Yeh, analyst for DRAMeXchange at TrenForce Corp.

This market report, published on May 26, 2021, was written by Ben Yeh, analyst for DRAMeXchange at TrenForce Corp.

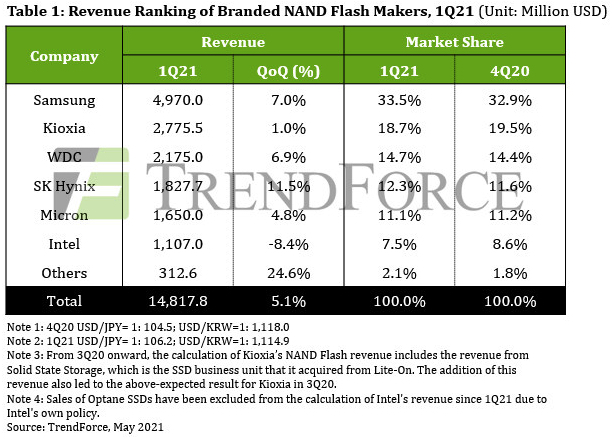

Total NAND flash revenue for 1Q21 increased by 5.1% Q/Q to $14.82 billion.

In particular, bit shipments rose by 11% Q/Q, while the overall ASP dropped by 5% Q/Q; hence, bit shipment growth offset the decline in the overall ASP.

Although NAND flash demand from notebook computer and smartphone manufacturers remained high, clients from the data center segment exhibited relatively weak demand, since this segment had yet to leave the state of NAND flash oversupply.

Contract prices for this quarter therefore still mostly showed a considerable Q/Q drop.

On the other hand, OEMs/ODMs of end products began to increase procurement of NAND flash products from the second half of January onward because they noticed that the shortage of NAND flash controller ICs was affecting the production of medium- and low-density storage products. Besides avoiding a possible supply crunch in the future, OEMs/ODMs were placing additional orders because they were preparing for a push to expand market share. On account of these developments, the overall NAND flash demand surpassed expectations in 1Q21.

Turning to 2Q21, factors on the supply and demand sides have turned oversupply into a shortage and propelled quotes upward for the mainstream categories of NAND flash products. On the supply side, the shortage of NAND flash controller ICs has worsened and resulted in a wider impact on the production of finished storage products. On the demand side, clients in the data center segment and OEMs of enterprise servers are ramping up component procurement. With prices rising and bit shipments growing, the quarterly total revenue is projected to register a Q/Q increase for 2Q21. However, in the long term, the continuation of the shortage of controller ICs may cause prices of NAND flash wafers to drop first and eventually constrain further revenue growth.

Samsung

Its NAND flash revenue went up for 1Q21 on account of several factors. First, smartphone brands and notebook OEMs began to release significant upside demand starting in the second half of January. Second, the demand for enterprise SSDs also grew as the previous quarter was a low base for comparison. NAND flash bit shipments for 1Q21 increased by nearly 12% Q/Q, exceeding the original projection of 10%. Although NAND flash ASP fell by 5% because the whole NAND flash market was still in a state of oversupply, its NAND flash revenue for 1Q21 still rose by 7.0% Q/Q to $4.97 billion.

Kioxia

It saw continuing growth in the sales of its SSDs in 1Q21 thanks to the strong demand for notebooks. However, SSD sales were not enough to wholly offset the previous decline in its mobile NAND flash sales. All in all, the supplier’s bit shipments grew by about 5% Q/Q for 1Q21. The general oversupply also led to a Q/Q drop of around 7% in its ASP. All in all, revenue rose slightly by 1.0% Q/Q to $2.78 billion. The calculation includes the revenue from the SSD business that Kioxia acquired from Liteon.

Western Digital

It recorded a Q/Q increase of 8% in its bit shipments for 1Q21 due to the strong notebook demand as well as brisk sales of its SSDs and retail storage products. However, its ASP dropped because contract prices for quarterly deals were arranged when the market was still in oversupply. the firm can respond quickly to the latest changes in price trends because a significant share of its sales mix is comprised of products for the retail market, the channel market, and memory module houses. Hence, its ASP fell by just 2% Q/Q for 1Q21. On the whole, NAND flash revenue reached $2.18 billion for 1Q21, up 6.9% from the previous quarter.

SK Hynix

Mobile-related products comprise a large share of its NAND flash shipments, so the increase in the stock-up demand from Chinese smartphone brands boosted revenue performance in 1Q21. Among NAND flash suppliers, the company recorded the highest Q/Q growth rate in bit shipments (i.e., 21%) for 1Q21. However, it also recorded a Q/Q drop of around 7% in its ASP because of the decline in contract prices and the issue of having high-density products account for a large share of its sales mix. On the balance, NAND flash revenue jumped 11.5% Q/Q to $1.83 billion for 1Q21.

Micron

Its bit shipments rose by nearly 10% Q/Q for its FY2Q21 (ended on March 4) due to stock-up activities by smartphone brands and notebook OEMs. It is noteworthy that QLC SSDs have been successfully incorporated into the gaming models of notebook OEMs, and this helps with the continuous growth of these particular products for the company. NAND flash ASP fell by roughly 3% Q/Q owing to the excess supply situation during quarterly contract negotiations. Taken altogether, NAND flash revenue rose by 4.8% Q/Q to $1.65 billion for 2FQ21.

Intel

Despite the inventory reduction for data centers and enterprise server OEMs during 1Q21, bit shipments continued to rebound thanks to the gradually recovering demand. Furthermore, the demand from PC OEMs remained vigorous. Hence, bit shipments grew by more than 10% Q/Q for 1Q21. However, the decline in contract prices of enterprise SSDs resulted in a Q/Q drop of around 4% in NAND flash ASP. It is noteworthy that the revenue figures announced by Intel will not comprise of Optane SSD and any 3D XPoint products starting from 1Q21. Thus, the company’s revenue came to $1.11 billion for 1Q21, down 8.4% from the previous quarter. There would be a Q/Q growth of 9.7% in revenue if the calculation includes only the “pure” NAND flash products (i.e., without 3D XPoint).

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter