Top 10 SSD Module Makers

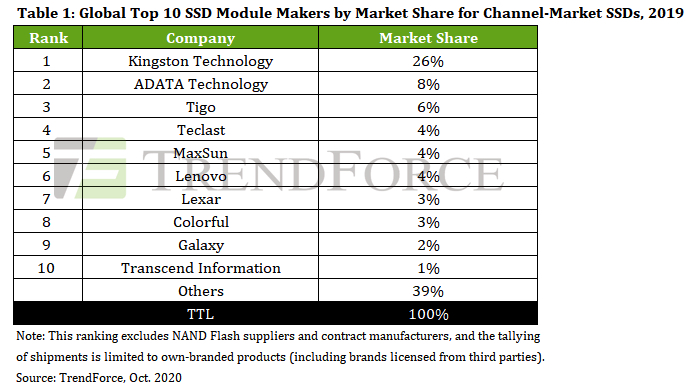

First 3 being Kingston, Adata and Tigo

This is a Press Release edited by StorageNewsletter.com on November 3, 2020 at 2:18 pmThe total WW shipments of branded SSDs bound for the channel (retail) market in 2019 reached 131 million units, showing an increase of almost 60% from 2018, according to TrendForce, Inc.

This result also indicated a further and substantial growth in SSD adoption. Kingston, Adata, and Tigo remained first, second, and third place respectively in the global ranking of branded SSD module makers (excluding NAND flash suppliers) by shipment market share for retail SSDs.

The ranking of SSD module makers for 2019 is based on the same criteria as before. Specifically, the shipment calculation only takes account of products that are bound for the channel market and under brands owned by manufacturers themselves (including brands licensed from third parties). NAND flash suppliers are excluded from the ranking in order to provide a better comparison of the shipment shares of the world’s top 10 branded SSD module makers.

Together, the top 10 accounted for around 61% of the total WW shipments in 2019. Looking at the channel market for SSDs as a whole, NAND flash suppliers (including Samsung, Kioxia, WDC, Micron, SK Hynix, and Intel) accounted for around 35% of the total shipments in 2019. The shipment share of SSD module makers (encompassing manufacturers of branded and white-box products) came to around 65% for the same year.

Taiwan-based Transcend fell to the 10th spot, while the Chinese landscape remained hypercompetitive, with major changes throughout the ranks

Kingston exploited the continuing slide in the overall ASP of NAND flash and operated vs. headwinds. Also, it has an extensive global network of sales channels, and its product support service is well developed. All these factors contributed to the cementing of the company’s position as the leader in the global shipment ranking, with a 26% market share in 2019.

ADATA is one of the few Taiwan-based SSD module makers that focus on the channel market. Last year, it kept building up the value of its brand and expanded its presence in the market for high-end hardware deployed in the e-sports scene. Moreover, the solutions that the company provides in the channel market are diverse and flexible in pricing. Owing to its strategy and wide selection of offerings, ADATA was able to post a growth in market share compared with 2018.

Most Chinese SSD module makers were impacted by a severe price slump in 2019. Some were unable to maintain a stable supply of products, while a few others exited the market altogether.

However, Tigo was a notable exception. The company already set up a well-functioning production system when it was first established, and it has developed a comprehensive product lineup. To further enhance its brand image and quality, Tigo also launched solutions for industrial applications in 2019. Hence, the company is still the leader among Chinese SSD module makers with respect to market share.

The 4th to 10th ranks on the top 10 list indicate the continued growth of the Chinese channel markets and the rising ranks of Chinese module makers. However, the fact that most of these companies possessed similar market shares also reflected the hypercompetitive state of the Chinese market, leading to more and more tier-two and tier-three companies exiting the market due to their inability to turn a profit.

On the other hand, Taiwanese suppliers’ shipment performances in the Chinese market were severely hampered by the rise of Chinese suppliers. As well, Taiwanese suppliers demonstrated a rather conservative channel market strategy, with only ADATA and Transcend making an appearance on the top 10 list. This would suggest that Taiwanese suppliers shifted their sales strategies to invest more resources into the industrial and OEM markets, potentially causing their market shares to plummet even further in the future.

Companies such as Goke continue to pursue market share in China amidst saturated SSD market

China-based suppliers MaxSun, Colorful, and Galaxy have all been established in the gaming market in China for years. Although the three companies had possessed a certain degree of brand recognition, they experienced difficulties in raising their shipment volumes because they were all competing in the relatively homogenous channel markets.

In particular, MaxSun was able to expand to various sales channels by fielding a diversified SSD product range; the company was therefore able to maintain an upward shipment trajectory.

Thanks to their comprehensive market channels, Teclast and Lenovo gradually increased their market shares and improved their rankings in 2019 compared to 2018.

After its acquisition by Longsys, Lexar went full steam ahead in the brand channel markets by aggressively utilizing Longsys’ resources. Lexar underwent a rapid growth in its shipment from the supply and pricing support provided by NAND flash suppliers and finally made an appearance in the top 10 list last year.

Making its debut on the top 10 list in 2018, Lite-On concluded its merger with Kioxia in July 2020. In order to maximize the group synergy from the merger, Lite-On will further streamline the entire range of its product lineup for the enterprise, PC OEM, and channel markets. With Kioxia providing pricing support and Lite-On’s in-house SSD IC R&D capabilities, Lite-On may likely return to the top 10 ranking in 2021 by making headways in the channel markets.

Likewise, as one of the heavyweights in the SSD module market in China, BIWIN has been cultivating its channel market strategies since receiving brand authorization from HP to become the latter’s official SSD and DRAM business partner. Going forward, It is expected to maintain a substantial potential for growth in the hypercompetitive Chinese market.

In addition to the aforementioned companies, numerous newcomers such as GOKE have been vying for a place in the vast Chinese market. GOKE is planning to release its own SSD products by leveraging its SSD controller IC R&D capabilities. The company hopes to establish a standing in the market through both product differentiation and localized manufacturing advantages.

Key upcoming trends in SSD market include the rise of PCIe interface and popularization of QLC architecture

In the future, the main focus of SSDs for the channel markets will gradually shift to PCIe and QLC, with PCIe’s performance stability in high-speed data transmissions becoming a basic requirement. In addition, given the intense competition among NAND flash suppliers in 2020, QLC SSD has seen a massive growth in shipment volumes. As suppliers gradually transition into processes above 128L, the cost advantage of QLC will attract more module makers to join the supply side of the market. With high-speed PCIe interface and quickly declining QLC costs both becoming future market trends, releasing relevant products ahead of market competitors will be the key to module makers’ success.

On the whole, TrendForce forecasts a 10% Y/Y shipment decline in the channel market for 2020. On the other hand, sluggish NAND flash prices are likely to persist in 2021 due to the oversupply situation in the market. After SK Hynix’s acquisition of Intel’s NAND flash business concludes and reshuffles the overall NAND market, the market shares of SSD module makers will potentially shift once again.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter