Covid-19 Had Greater Impact on Established NAND Manufacturers

As Chinese YMTC aims to mass produce 128L products by end of year.

This is a Press Release edited by StorageNewsletter.com on April 28, 2020 at 2:34 pmAccording to the DRAMeXchange research division of TrendForce, Inc., Chinese NAND flash manufacturer YMTC submitted samples of its 128L 3D NAND products to storage controller chip suppliers in 1Q20.

The company is aiming to begin wafer input in 3Q20 and start mass production by the end of the year.

The initial applications being considered for the 128L process include UFS-based storage solutions and SSDs; YMTC also intends on shipping packaged dies and wafers based on this technology to module houses. Factoring in the time for adoption among OEM clients, TrendForce believes that YMTC’s 128L production could first affect contract prices of NAND wafers as early as 4Q20. Then, YMTC is expected to apply its 128L process to client SSDs, eMMC/UFS solutions, and other storage products starting from 2021. With the Chinese manufacturer poised to expand the overall supply with its latest technology, the possibility of declining prices next year has become higher for most types of NAND flash products.

The demand for end products, including smartphones and notebook computers (laptops), will be affected in the near future on account of the Covid-19 pandemic. For the established NAND flash suppliers, this turn for the worse is expected to impede their profitability and constrain their future capacity expansion efforts.

In comparison, given YMTC’s relatively low market share across NAND flash storage applications at the moment, the company will not be as directly affected by the fallout from the pandemic as the established manufacturers.

As for strategic aims, YMTC will be concentrating on two things: (1) improving the yield rate of its 64L TLC process along with raising the adoption of its 64L TLC products by OEMs; and (2) getting its 128L approved by prospective customers as soon as possible within this year. To grow its client base, YMTC has included both the TLC and QLC architectures in its 128L samples.

Gradual increase in difficulty of 3D NAND stacking

benefits YMTC in minimizing competitive gaps

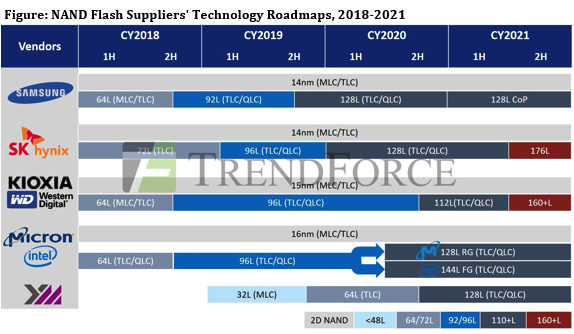

As the stacking of 3D NAND flash reaches more than 90L, it becomes progressively difficult for the major suppliers in developing higher layers of etching and stacking technology. Observation on suppliers’ technology roadmaps finds that there are already differences among suppliers with respect to the gen of the 1XX L stacking. While Samsung and SK Hynix have already released their 128L products, Kioxia/WD, Micron, and Intel will have to wait until 2H20 to drastically increase production for their 112/128/144L products. The development of 1XX L products takes a longer period compared to the progressive pattern for previous gens of 3D NAND products, thus benefiting YMTC in catching up to the existing competition with its 128L products.

In addition, the overall NAND flash ASP sustained a Y/Y drop of 46% in 2019, in turn inducing losses for the established suppliers and prompting them to adopt a conservative CapEx, with a record low output growth planning. This phenomenon has given YMTC an opportunity to bridge the competitive gap.

YMTC’s production capacity is projected

to occupy about 8% of the total NAND flash output in 2021

The new supplier currently operates a manufacturing site in Wuhan, China, whereas its Chengdu fab is expected to enter production within the year. It intends to steadily complete the construction and production expansion of the two remaining fabs at the Wuhan site. Aside from its aggressive expansion plans, it is also a key manufacturer cultivated under the Big Fund, China’s national semiconductor fund. Its increased participation in the NAND flash market is expected to elevate the severity of the competition, resulting in a continuous price reduction in the long run.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter