Nutanix: Fiscal 4Q18 Financial Results

Now more than one billion company, but with $297 million yearly net loss

This is a Press Release edited by StorageNewsletter.com on September 3, 2018 at 2:34 pm| (in $ million) | 4Q17 | 4Q18 | FY17 | FY18 |

| Revenue | 252.5 | 303.7 | 845.9 | 1,155 |

| Growth | 20% | 37% | ||

| Net income (loss) | (66.1) | (87.4) | (379.6) | (297.2) |

Nutanix, Inc. announced financial results for its fourth quarter and fiscal year ended July 31, 2018.

4FQ18 Financial Highlights

• Revenue: $303.7 million (at 77.7% non-GAAP gross margin), up from $252.5 million (at 62.6% non-GAAP gross margin) in 4FQ17, reflecting the elimination of approximately $95 million in pass-through hardware revenue in the quarter as the company continues to execute its shift toward increasing software revenue (1)

• Software and Support Revenue: $267.9 million, growing 49% Y/Y from $179.6 million in 4FQ17

• Billings: $395.1 million, growing 37% year-over-year from $289.2 million in 4FQ17

• Software and Support Billings: $359.2 million, growing 66% year-over-year from $216.3 million in 4FQ17

• Gross Margin: GAAP gross margin of 75.9%, up from 61.4% in the fourth quarter of fiscal 2017; Non-GAAP gross margin of 77.7%, up from 62.6% in 4FQ17

• Net Loss: GAAP net loss of $87.4 million, compared to a GAAP net loss of $66.1 million in the fourth quarter of fiscal 2017; Non-GAAP net loss of $19.0 million, compared to a non-GAAP net loss of $26.0 million in 4FQ17

• Net Loss Per Share: GAAP net loss per share of $0.51, compared to a GAAP net loss per share of $0.43 in the fourth quarter of fiscal 2017; Non-GAAP net loss per share of $0.11, compared to a non-GAAP net loss per share of $0.17 in 4FQ17

• Cash and Short-term Investments: $934.3 million, up 168% from 4FQ17

• Deferred Revenue: $631.2 million, up 71% from 4FQ17

• Operating Cash Flow: $22.7 million, compared to $5.9 million in 4FQ17

• Free Cash Flow: $6.5 million, compared to negative free cash flow of $6.5 million in 4FQ17

Fiscal Year 2018 Financial Highlights

• Revenue: $1.16 billion (at 68.1% non-GAAP gross margin), up from $845.9 million (at 63.1% non-GAAP gross margin) in fiscal 2017, reflecting the elimination of approximately $169 million in pass-through hardware revenue in fiscal 2018 as the company continues to execute its shift toward increasing software revenue (1)

• Software and Support Revenue: $898.1 million, growing 47% Y/Y from $609.6 million in fiscal 2017

• Billings: $1.42 billion, growing 43% year-over-year from $990.5 million in fiscal 2017

• Software and Support Billings: $1.16 billion, growing 54% year-over-year from $754.2 million in fiscal 2017

• Gross Margin: GAAP gross margin of 66.6%, up from 61.3% in fiscal 2017; Non-GAAP gross margin of 68.1%, up from 63.1% in fiscal 2017

• Net Loss: GAAP net loss of $297.2 million, compared to a GAAP net loss of $379.6 million in fiscal 2017; Non-GAAP net loss of $101.5 million, compared to a non-GAAP net loss of $120.7 million in fiscal 2017

• Net Loss Per Share: GAAP net loss per share of $1.81, compared to a GAAP net loss per share of $2.96 in fiscal 2017; Non-GAAP net loss per share of $0.62, compared to a pro forma non-GAAP net loss per share of $0.85 in fiscal 2017

• Operating Cash Flow: $92.6 million, compared to $13.8 million in fiscal 2017

• Free Cash Flow: $30.2 million, compared to negative free cash flow of $36.4 million in fiscal 2017

“We ended the year on a high note with a record quarter on many fronts, positioning us extremely well for the future. We will continue to invest in talent and hybrid cloud technology while incubating strategic multi-cloud investments such as Netsil, Beam, and now Frame,” said Dheeraj Pandey, chairman, founder and CEO. “Frame increases our addressable market, brings another service to our growing platform, and adds employees with insurgent mindsets who will help us continue to challenge the status quo.”

“The company’s strong achievement of 78% non-GAAP gross margin, the best in our history, is the direct result of our successful execution toward a software-defined business model,” said Duston Williams, CFO. “We’re also tracking above our target performance we set using the ‘Rule of 40’ framework, demonstrating our ability to balance growth and cash flow.”

Recent company Highlights

• Completed the Acquisition of Frame: Frame, in cloud-based Windows desktop and application delivery, increased the company’s addressable market. IDC estimates that the desktops-as-a-service software market is forecast to grow to $3 billion in 2021 at a CAGR of 32%. With the addition of Frame, customers will be able to deliver desktops-as-a-service from multiple clouds, combining the consumer-grade simplicity and web-scale design of cloud applications with the functionality of traditional virtual desktop applications.

• Achieved Milestone of $1 Billion+ in Annual Revenue in Less Than a Decade from Inception: Grew fiscal 2018 revenue to $1.16 billion, excluding $169 million in pass-through hardware revenue eliminated, crossing the $1 billion milestone.

• Expanded Customer Base Hitting Milestone 10,000+ Customers and Signed Largest Deal in History: The company ended the fourth quarter of fiscal 2018 with 10,6103 end-customers, adding 1,000 new end-customers in the quarter. Notably, the company passed a milestone, adding its 10,000th customer during the quarter. It also expanded an existing customer engagement by closing a deal greater than $20 million in the quarter, the largest in firm’s history.

• Successfully Continued Transition to a Software-Defined Business Model: Grew software and support billings by 66% Y/Y in the fourth quarter. Pass-through hardware billings decreased to 9% of total billings in the quarter, down from 25% in the fourth quarter of fiscal 2017.

• Launched 12 Culture Principles Representative of company Values: Codified the company’s corporate values with the articulation and launch of 12 culture principles. These principles serve as the foundation for how employees work with each other, with partners, and with customers.

• Added Two New Executives in Key Functions: Prabha Krishna joined Nutanix as the SVP of people and places, and is responsible for the HR and facilities teams worldwide. In addition, Ben Ravani joined as the SVP of Xi reliability engineering to oversee building and operating Xi Cloud Services as well as serve as the GM of the Nutanix Seattle site.

• Introduced New Velocity Program for Scaling Growth in the Mid-Market: The company launched its Velocity channel program in June, aimed at accelerating the selling processes, incentives, and marketing investments for strategic, mid-market focused channel partners. The program provides a frictionless experience for channel partners, giving them more leverage to grow their business.

• Expanded its Global Workforce: The vendor has rapidly increased and evolved its operations in India over the past five years and recently ranked second on India’s Great Mid-Size Workplaces 2018 list. Additionally, the company continues to increase its headcount in Bangalore, Belgrade and Berlin as it further disrupts traditional enterprise IT incumbents with an increasingly global workforce.

• Certified as the First Hyperconvergence-Based Solution for SAP HANA: In August, the company received certification from SAP for its AHV hypervisor and Enterprise Cloud OS platform as the first hyperconverged infrastructure solution to pass SAP’s criteria for running production SAP HANA deployments. With this achievement, customers combine the cost and operational benefits of modernized IT infrastructure with the scale and performance required for SAP HANA. For Nutanix, this presents an opportunity to broaden penetration in Global 2000 accounts.

For 1FQ19, Nutanix expects:

• Revenue between $295 and $310 million, implying software and support revenue growth of approximately 40-45% Y/Y;

• Billings between $370 and $390 million, implying software and support billings growth of 50-55% Y/Y;

• Bill-to-revenue ratio of approximately 1.26x;

• Non-GAAP gross margin between 78% and 79%;

• Non-GAAP operating expenses between $280 and $290 million;

• Non-GAAP loss per share between $0.26 and $0.28, using approximately 176 million weighted shares outstanding

First quarter guidance reflects a faster removal of pass-through hardware than originally anticipated, accelerating the reduction of zero margin billings and revenue with the benefit of improved gross margins. Additionally, the Q1 expected bill-to-revenue ratio of 1.26x is higher than street consensus of 1.21x, implying an approximate $12 million in deferred revenue that would have otherwise been in revenue and gross profit.

(1) The elimination of hardware revenue is based on the estimated cost of hardware in transactions where our customers purchase such hardware directly from our contract manufacturers.

Comments

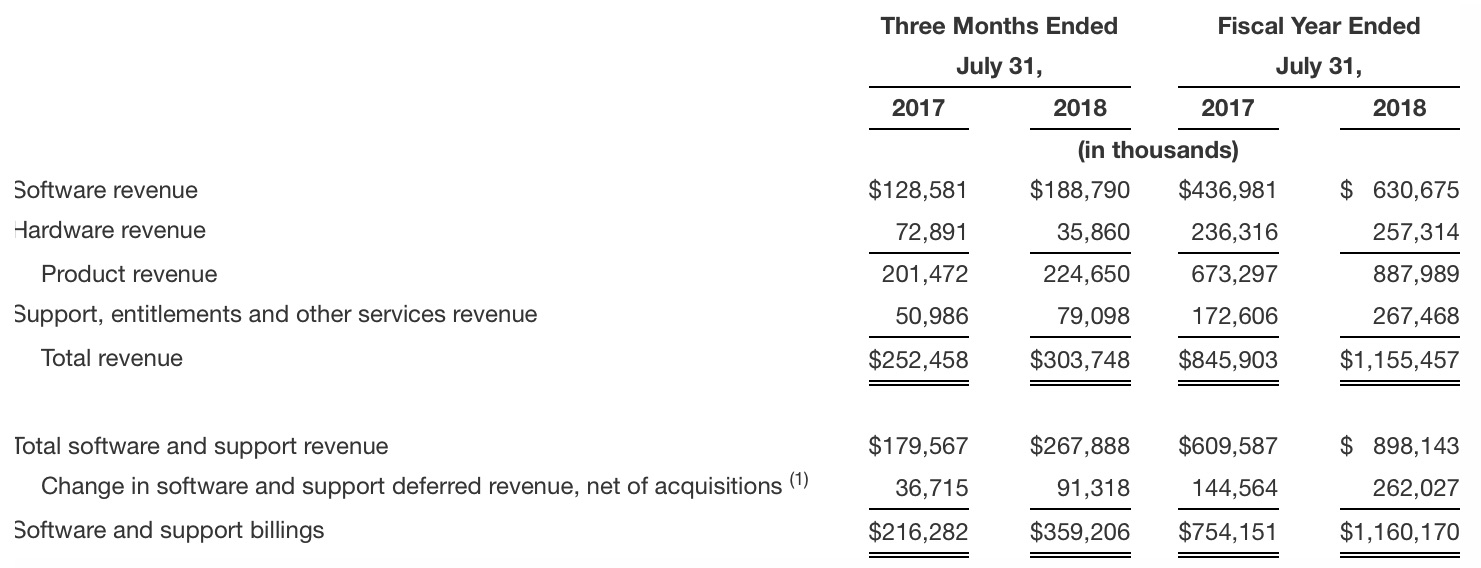

Disaggregation of Revenue and Reconciliation

of Software and Support Revenue to Software and Support Billings

Click to enlarge

(1) Amount for the fiscal year ended July 31, 2017 excludes approximately $6.0 million of deferred revenue assumed in the PernixData acquisition. Amount for the twelve months ended July 31, 2018 excludes $0.1 million of deferred revenue assumed in an acquisition.

(1) Amount for the fiscal year ended July 31, 2017 excludes approximately $6.0 million of deferred revenue assumed in the PernixData acquisition. Amount for the twelve months ended July 31, 2018 excludes $0.1 million of deferred revenue assumed in an acquisition.

Since its inception, Nutanix, now with 4,010 employees, continues to trade off free cash flow and profitability in favor of extending market share.

It explains company's impressive growth surpassing $1 billion after less than ten years of business with continuing net losses. And the firm is not going to change this model for next fiscal year.

Remember that, in last FY18, Nutanix embarked on a business and consumption model transition focusing on the elimination of the pass-through hardware revenue associated with the sales of its appliances.

In FY18, the company delivered close to $1.2 billion in software and support billings, growing 54% year-over-year and added over 3,600 new customers.

For the most recent quarter global sales reached $303.7 million, 5% Q/Q and 20% Y/Y, ahead of guidance of $295 million to $300 million.

For this quarter, it got 46 deals worth more than $1 million; 9 of which at more than $3 million and 2 at more than $5 million.

In this last fiscal year, it added nearly as many customers as it had when it went public two years ago. It now count 710 Global 2000 companies as customers, adding approximately 40 in 4Q18 and 140 in FY18.

It closed 201 deals worth more than $1 million in FY18, up from 144 in FY17, and has 26 customers with a lifetime spend of more than $10 million, up from 11 in the former fiscal year.

Its top deal of the quarter and the largest in the company's history worth more than $20 million was with a DoD agency - name not revealed - looking for a solution to power its combat edge clouds across the world. This customer will use Nutanix Enterprise Cloud platform to power 15 remote sites running two different networks.

For 1FQ19, Nutanix expects once more a low quarterly growth, between -3% and +2%.

To read the earnings call transcript

Read also:

Nutanix: Fiscal 3Q18 Financial Results

One of WW fastest growing storage company but not able to be profitable

2018.05.28 | Press Release | [with our comments]

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter