Storage Start-Ups in 2017

VCs investing 34% more than in 2016

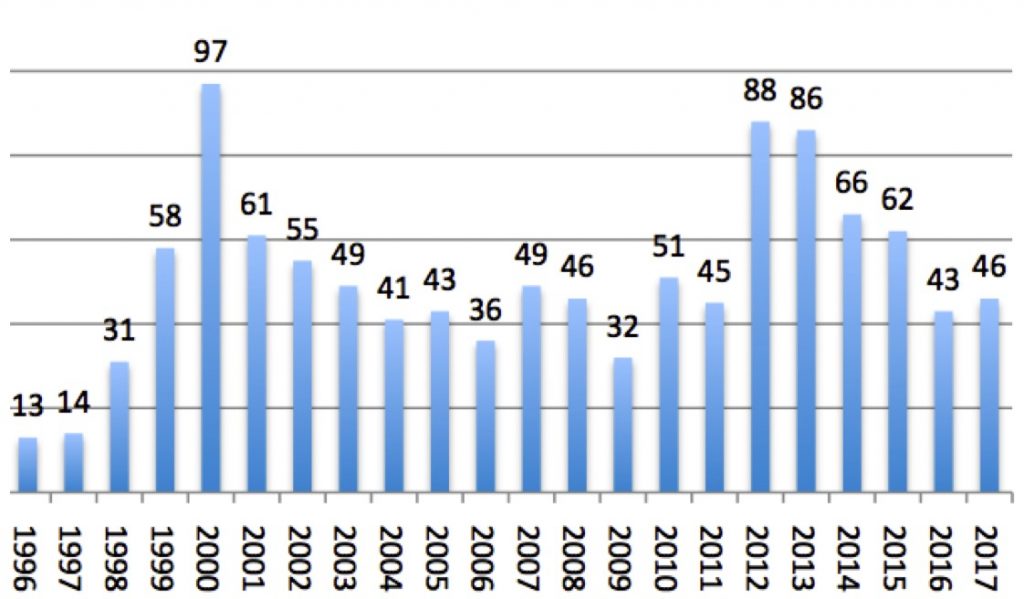

By Jean Jacques Maleval | February 1, 2018 at 2:30 pm2017 was a little better than 2016 for storage start-ups. VCs were less reluctant to invest in storage. There were 46 financial rounds last year compared to 43 in 2016, that was the lowest figure since 2009, for a total amount of $1,256 million up 34% Y/Y.

The highest round was $180 million for Rubrik, $77 million for Upthere in 2016, $175 million for Simplivity in 2015, and $900 million for Cloudera in 2014.

NUMBER OF FINANCIAL ROUNDS FROM 1996 TO 2017

(Source: StorageNewsletter.com)

LARGEST FINANCIAL ROUNDS IN 2017

(at $50 million and more)

| Company | in $ million |

| Rubrik | 180 |

| Infinidat | 95 |

| Cohesity |

90 |

| Druva |

80 |

| Oodrive | 69 |

| MapR | 56 |

| Vexata |

54 |

(Source: StorageNewsletter.com)

There was 7 rounds at more than $50 million last year and 8 in 2016. Rubrik was n°3 in 2016 with $61 million with now a total at $292 million. Kaminario also surpasses $200 million in 2017 in total funding with $218 million.

Why only a little better in 2017?

The worldwide storage market is no more growing and then not a real good opportunity for investors. Furthermore the more popular technologies attracting users (SSDs, all-flash systems, software-defined storage, scale-out NAS, hyperconverged platform, cloud storage), there are already too many competitors including about all storage giants.

Furthermore, there is currently about no new killer technology that could convince VCs, just improvements.

More New Start-Ups

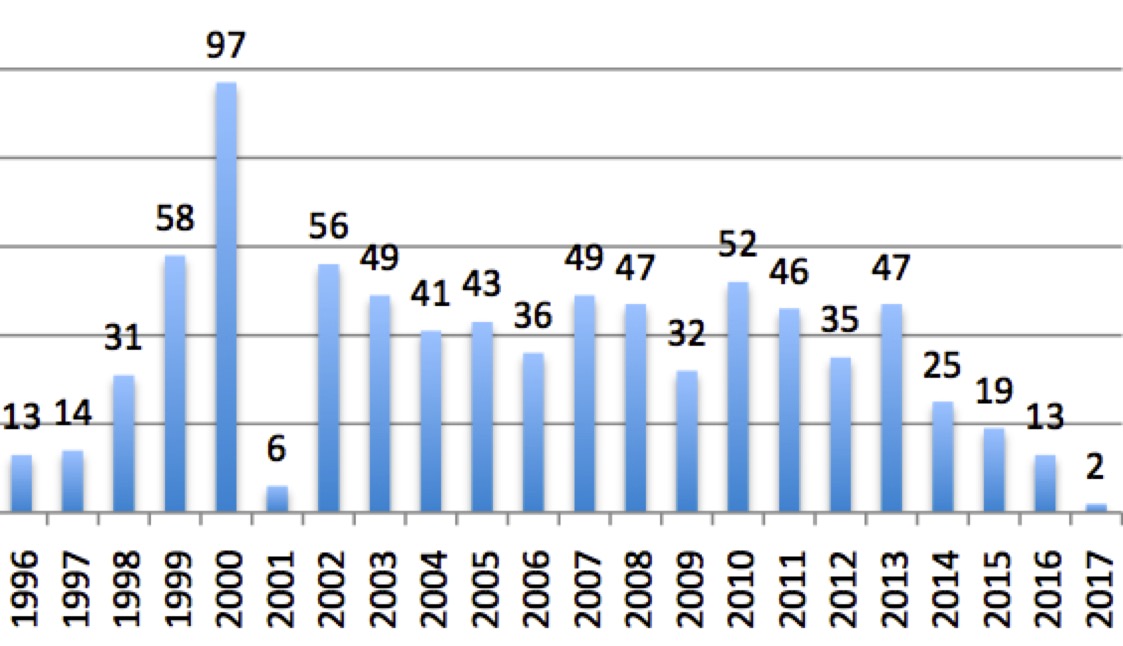

Also worrying is the reduced number of start-ups founded since the heydeys of 2000 when 97 new entities sprang up in a single year. We were only able to turn up 2 new firms launched last year vs. 13 in 2016, 19 in 2015 and 25 in 2014, while these figures will go up as more of them, operating in stealth mode, will come to light. For example, we found only 4 born firms in 2016 at the same time last year, this figure being increased by 9 more entities discovered later.

NUMBER OF STORAGE START-UPS LAUNCHED EACH YEAR SINCE 1996

(when the born year is known)

(Source: StorageNewsletter.com)

2017 Good Year in Financial Funding

The average amount per round increases yearly 23%, from $22 million to $27 million.

Investors put more money in more start-ups.

These past 14 years, VCs have put $24.8 billion in storage start-ups. This amount is much higher than the total figure in the table below ($17.8 billion adding all rounds) because, for several firms, we got the total invested but not the details per round.

On average, a company got historically $46 million in total funding, the average per round being $18 million.

ALL FINANCIAL ROUNDS FROM 2003 TO 2017

(only for start-ups releasing the amount of their financial rounds)

| Year | Number of rounds |

Total invested* |

Average per round* |

| 2003 | 57 | 759 | 13 |

| 2004 | 78 | 990 | 13 |

| 2005 | 80 | 1,004 | 13 |

| 2006 | 68 | 818 | 12 |

| 2007 | 68 | 789 | 12 |

| 2008 | 58 | 818 | 14 |

| 2009 | 59 | 591 | 10 |

| 2010 | 69 | 865 | 13 |

| 2011 | 70 | 1,235 | 18 |

| 2012 | 88 | 1,499 | 17 |

| 2013 | 86 | 1,635 | 19 |

| 2014 | 66 | 2,882 | 44 |

| 2015 | 62 | 1,741 | 28 |

| 2016 | 43 | 937 | 22 |

| 2017 | 46 | 1,256 | 27 |

| TOTAL | 998 | 17,819 | 18 |

* in $ million

(Source: StorageNewsletter.com)

TOTAL INVESTED IN START-UPS FROM 2003 TO 2017 ALL ROUNDS INCLUDED

(only for companies releasing total amount invested)

| Total invested* | 24,811 |

| Number of start-ups | 534 |

| Average per start-up* | 46 |

* in $ million

(Source: StorageNewsletter.com)

PER ACTIVITY AMONG CURRENT 527 ALIVE START-UPS

| Activity | Number | % |

| Software | 249 | 47% |

| Hardware | 143 | 27% |

| SSP, cloud |

81 | 15% |

| Connection | 28 | 5% |

| Fundamental technology | 19 | 4% |

| Security | 7 | 1% |

| TOTAL | 527 | 100% |

(Source: StorageNewsletter.com)

Where Are They Going?

What becomes of all these storage start-ups after we identify and count them. The conclusion is not really reassuring, a reminder that investment in these sorts of companies is in fact highly risky.

On all start-ups identified, only 4% eventually go public, and thus allow investors generally more than just to recoup their original stake. The same is generally true for the 28% that find buyers, although the asking price is not always greater than the total of all sunk investments. It is, in any case, the emergency exit that many companies are seeking. Meanwhile, another 18% just vanish off the map – doors closed.

52% of all alive start-ups remain in a holding pattern, still a start-up, still nursing the secret hope of an offer from a storage giant seeking to fill-in a missing technology.

WHAT HAPPENED TO THEM SINCE 1978

(out of a total 950 start-ups)

| Became public | 34 | 4% |

| Sold | 267 | 28% |

| Closed | 170 | 18% |

| Remaining start-ups | 490 | 52% |

NB: Total here is 961 – and not 950 – because 11 firms became public AND/OR were sold AND/OR were closed.

(Source: StorageNewsletter.com)

18 two start-ups did find buyers or merged in 2017, 4 in 2016 and 13 in 2015, the biggest deal last year being Barracuda Networks sold to Thoma Bravo for $1.6 billion. Record in 2016 was SolidFire acquired by NetApp for $870 million. HPE was an avid acquirer in 2017, buying Nimble Storage for $1.09 billion and SimpliVity for $650 million.

There was just 4 IPOs in 2015 and 2 in 2016 (EverSpin Technologies and Nutanix) and 2 in 2017: Cloudera raising $225 million and Tintri $60 million, much less than total financial funding, $1.04 billion and $260 million respectively. Pure Storage raised $450 million in 2014 and Box $554 million in 2015, the highest sum never received by a storage company becoming public. Here are some start-ups eventually able to enter into the stock exchange: Acronis, Dropbox, DataCore, Exagrid, Infinidat, Kaminario, MapR, Nasuni, Rubrik, Scality, Veeam.

These facts demonstrate that, to get more money to finance the growth of young companies, IPO seems today a better way than an acquisition.

35 IPOs IN STORAGE INDUSTRY

| Company | IPO year | Amount raised* | Total funding* |

| Silicon Storage Technology |

1995 | 15 | NA |

| StorageNetworks | 2000 | 260 | 205 |

| BakBone | 2000 | NA | NA |

| McData | 2000 | 350 | NA |

| STEC | 2000 | 65 | NA |

| FalconStor** | 2001 | NA | 33 |

| Xyratex | 2004 | 48 | NA |

| Rackable Systems | 2005 | 75 | 21 |

| CommVault | 2006 | 161 | 75 |

| Double-Take | 2006 | 55 | 70 |

| Isilon | 2006 | 108 | 69 |

| Riverbed | 2006 | 86 | 38 |

| 3PAR | 2007 | 95 | 183 |

| Compellent | 2007 | 85 | 53 |

| Data Domain | 2007 | 111 | 41 |

| Mellanox | 2007 | 102 | 89 |

| Netezza | 2007 | 124 | 68 |

| Voltaire | 2007 | 47 | 75 |

| Rackspace Hostings | 2008 | 145 | NA |

| OCZ Technology | 2010 | 101 | NA |

| Carbonite | 2011 | 62 | 67 |

| Fusion-io | 2011 | 223 | 112 |

| JCY International | 2011 | 238 | NA |

| Parade Technologies | 2011 | 34 | 21.5 |

| Violin Memory | 2013 | 162 | 186 |

| Nimble Storage | 2013 | 168 | 99 |

| Barracuda Networks | 2013 | 75 | 40 |

| Hortonworks | 2014 | 110 | 173 |

| Adesto Technologies | 2015 | 22 | 54 |

| Box | 2015 | 554 | 175 |

| Mimecast | 2015 | 83 | 77.5 |

| Pure Storage | 2015 | 470 | 425 |

| EverSpin Technologies | 2016 | 40 | 45 |

| Nutanix | 2016 | 238 | 370 |

| Tintri | 2017 | 60 | 260 |

| Cloudera | 2017 | 225 | 1,041 |

| Average of known figures | 140 | 140 |

* in $ million

** became public via a merger with Network Peripherals

(Source: StorageNewsletter.com)

WHERE DO 490 CURRENT ALIVE START-UPS COME FROM

Storage is mainly an US sport.

| Countries | Number of start-ups |

% |

| USA | 343 | 70% |

| UK | 22 | 4% |

| France | 20 | 4% |

| Canada | 16 | 3% |

| Israel* | 13 | 3% |

| India | 7 | 1% |

| Switzerland | 7 | 1% |

| Australia | 6 | 1% |

| China | 6 | 1% |

| Others | 50 | 10% |

| Total | 490 | 100% |

* Several start-ups were funded in Israel but transferred HQs in USA

(Source: StorageNewsletter.com)

HISTORICAL RECORDS IN TOTAL FINANCIAL FUNDING

(more than $200 million, no one in 2016, four more in 2017)

| Start-ups | Total financial funding* |

| Cloudera | 1,041 |

| Box | 554 |

| Pillar Data Systems | 544 |

| Pure Storage | 470 |

| Nutanix | 370 |

| Infinidat | 325 |

| Rubrik | 292 |

| SimpliVity | 276 |

| Tintri | 260 |

| Dropbox | 257 |

| MapR | 250 |

| Pivot3 | 247 |

| BlueArc | 224 |

| Kaminario | 218 |

| Actifio | 207 |

| StorageNetworks | 205 |

| Sanrise | 203 |

* in $ million

New entrants in 2017

(Source: StorageNewsletter.com)

13 NEW START-UPS (known thus far) BORN IN 2016

| COMPANY (HQ) |

BUSINESS |

| Aparavi Software (Santa Monica, CA) |

storage agnostic software as a service for long-term data retention; sister company of NovaStor |

| Atavium (Minneapolis, MN) | data management and cloud |

| Blockade Technologies (Boca Raton, FL) |

blockchain-based storage offered as cloud service |

| Envemio (Laguna Niguel, CA) | I/O Internet controller cards, then for IB and FC |

| LucidLink (San Francisco, CA) |

cloud backed distributed file service |

| Nextcloud (Stuttgart, Germany) |

open source file sync and share |

| Open vStorage (Lochristi, Belgium) |

elastic block storage system that is policy driven, multi-datacenter, multi-cloud with built-in self healing and backup |

| RStor.io (Los Gatos, CA) | in stealth mode |

| Simply (Los Angeles, CA) |

high-speed storage solutions for media professionals; out of stealth mode in 2016 |

| Sonora Labs (Aix-en-Provence, France) |

Lolas NAS to exchange storage resources to establish content delivery network |

| StrongBox Data Solutions (Montreal, Canada) | data management and storage solutions; acquired StrongBox product business from Crossroads Systems in April 2016; also in Germany |

| Vast data (Israel) | in stealth mode; big data and cloud storage; also in USA |

| Wasabi Technologies (Boston, MA) |

formerly BlueArchive; cloud-based, object storage as a service |

(Source: StorageNewsletter.com)

2 NEW START-UPS (known thus far) BORN IN 2017

| COMPANY (HQ) |

BUSINESS |

| Esoptra (Herentals, Belgium) | customizable, ultralight information access and integration |

| L2 Drive (Irvine, CA) | HDD technology |

ALL 46 FINANCIAL ROUNDS IN 2017

| COMPANY (HQ) | BORN IN | INVESTMENT IN 2017* | TOTAL INVESTMENT* | BUSINESS | |

| Atavium (Minneapolis, MN) |

2016 | 8.65 | 8.65 | data management and cloud | |

| Avere Systems (Pittsburgh, PA) |

2008 | 14 | 97 | tiered NAS appliances | |

| Bitglass (Campbell, CA) | 2013 | 45 | 80 | data protection on cloud for mobile devices | |

| Burlywood (Longmont, CO) |

2015 | 3.6 | 3.7 | modular controller architecture that accelerates time-to-market of new NAND adoption; two rounds in 2017 | |

| Chaos Sumo (Boston, MA) | 1 | NA | turning Amazon S3 into “smart object storage” | ||

| CNEX Labs (San Jose, CA) | 2013 | 23 | 60 | NVMe PCIe SSD controller | |

| Cohesity (San Jose, CA) | 2013 | 90 | 160 | web-scale, converged storage to unify backup, DevOps, and analytics | |

| Diamanti (San Jose, CA) | 2014 | 18 | 30.5 | network and storage solutions for Linux containers; formerly Datawise.io | |

| Diamond (San Mateo, CA) | NA | 2 | NA | single access point for all cloud-based email, storage services and personal devices | |

| Druva Software (Sunnyvale, CA) |

2007 | 80 | 198 | continuous data availability and de-dupe backup software for laptops; investment of NTT in 2016 | |

| Elastifile (Santa Clara, CA) | 2013 | 16 | 74 | software-defined storage solution for all-flash, distributed file, object, and block store and serving as enterprise scale out primary storage; R&D in Herzliya, Israel | |

| Excelero (Tel Aviv, Israel) | 2014 | 10 | 30 | software product that leverages, NVMe SSD and SR-IOV and RDMA; also in Santa Clara, CA | |

| Hedvig (Santa Clara, CA) | 2012 | 21.5 | 52 | software-defined storage system for cloud | |

| Iguaz.io (Herzliya, Israel) | 2014 | 33 | 48 | data management and storage solutions for big data, IoT and cloud applications | |

| Infinidat (Herzliya Pituach, Israel) |

2011 | 95 | 325 | High-end enterprise storage systems; Dr. Alex Winokur one of the founders; Moshe Yanai board’s director; also in Needham, MA | |

| Kaminario (Needham, MA) | 2008 | 75 | 218 | all-flash arrays; R&D in Israel | |

| Komprise (Campbell, CA) | 2014 | 12 | 18 | software using analytics-driven adaptive automation to manage massive data growth transparently across all storage silos | |

| L2 Drive (Irvine, CA) | 2017 | 0.5 | NA | HDD technology | |

| Leonovus (Ottawa, Canada) |

2008 | 2.8 | NA | software-defined object storage solution; 1.3 million and 1.5 million in 2017 | |

| Liqid (Lafayette, CO) | 2013 | 10 | 20 | on-demand composable infrastructure | |

| Mangstor (Austin, TX) | 2011 | 7.1 | 32 | PCIe flash controller | |

| MapR Technologies (San Jose, CA) |

2009 | 56 | 250 | distribution for Apache Hadoop for data protection and business continuity; R&D in India | |

| Minio (Palo Alto, CA) | 2014 | 20 | NA | for developers to build their own cloud storage | |

| Nasuni (Natick, MA) | 2009 | 38 | 120 | secure cloud storage; founded by former executives of Archivas | |

| Nexenta Systems (Santa Clara, CA) |

2005 | 20 | 161.5 | software-defined storage OS based on Linux and ZFS | |

| Oodrive (Paris, France) | 2000 | 69 | NA | storage provider with a SaaS platform; acquired Active Circle in 2014 | |

| OpenIO (Lille, France) | 2015 | 5 | 5.2 | open source object storage solution for massive storage infrastructures; office in San Francisco, CA |

|

| OwnBackup (Fort Lee, NJ) | 2012 | 7.5 | 11 | backup and restore ISV on the Salesforce.com AppExchange; also in Israel | |

| Panzura (Campbell, CA) | 2008 | 32 | 90 | cloud as storage tier integrated into interwoven global file system and global namespace | |

| Portworx (San Francisco, CA) |

1983 | 20 | 28.5 | software-defined infrastructure for containerized applications | |

| Primary Data (Palo Alto, CA) |

2013 | 20 | 83 | software-defined storage; merged with Tonian Systems in 2013; office in Israel; $20 million line of credit in 2017 | |

| Qumulo (Seattle, WA) | 2012 | 30 | 130 | modern scale-out file storage | |

| Reduxio Systems (San Francisco, CA) |

2012 | 22.5 | 47.5 | enterprise hybrid storage with 1-second data recovery, in-line in-memory de-dupe and compression and block-level tiering; also in Petach Tikvah, Israel | |

| Rubrik (Palo Alto, CA) | 2014 | 180 | 292 | scale-out storage architecture for backup | |

| ScaleMP (Fort Lee, NJ) | 2002 | 10 | NA | virtualization solutions for high-end computing | |

| SoftIron (London, UK) | 2012 | 7 | NA | HyperDrive software-defined storage portfolio built on Ceph | |

| SpinBackup (San Francisco, CA) |

2013 | 0.5 | 0.5 | cloud-to-cloud backup and cloud cybersecurity solutions | |

| StorageOS (London, UK) | 2015 | 2 | NA | low entry point, full enterprise functionality storage array integrated with VMWare, Docker, AWS, and Google Cloud | |

| Storj Labs (Atlanta, GA) |

2014 | 3 | 5.4 | decentralized, end-to-end encrypted cloud storage solution to use blockchain technology and cryptography to secure files | |

| StrongBox Data Solutions (Montreal, Canada) | 2016 | 27 | NA | data management and storage solutions; acquired StrongBox product business from Crossroads Systems in April 2016; also in Germany | |

| Tegile Systems (Newark, CA) |

2009 | 33 | 178 | multi-protocol SSD/HDD array with de-dupe for primary storage; acquired by Western Digital in 2017 | |

| Trilio Data (Hopkinton, MA) |

2013 | 5 | 5 | OpenStack backup, recovery and migration solutions | |

| Ugloo (Amiens, France) | 2015 | 1.3 | 1.9 | backup solution of distributed data | |

| Vexata (San Jose, CA) | 2013 | 54 | 103 | SSD real time array | |

| Wasabi Technologies (Boston, MA) | 2016 | 8.5 | 19.3 | formerly BlueArchive; cloud-based object storage as a service; two rounds in 2017: $8.5 and $10.8 million | |

| XSky (Hong Kong, China) |

2015 | 17 | 27 | distributed block storage solution for enterprises and carrier grade software-defined-storage product for cloud service providers and private cloud customers | |

* in $ million

(Source: StorageNewsletter.com)

Note: when there are more than one round of financial funding the same year, we add them considering the total as only one round.

Read also:

Storage Start-Ups in 2016

Worst year since 2003

by Jean Jacques Maleval | 2017.01.10 | News

Storage Start-Ups in 2015

Worst year since 2003 in number of financial rounds

by Jean Jacques Maleval | 2016.01.06 | News

Storage Start-Ups in 2014

Historical record for just one financial round: $900 million for …

by Jean Jacques Maleval | 2015.03.03 | News

Storage Start-Ups in 2013

$1.3 billion invested in 57 companies following 58 financial rounds

by Jean Jacques Maleval | 2014.01.08 | News

Storage Start-Ups in 2012

Innovation never stopping in industry, 67 new rounds last year

by Jean Jacques Maleval | 2013.02.13 | News

ANALYSIS: Storage Start-Ups in 2011

Record year in total financial funding: more than $1 billion

by Jean Jacques Maleval | 2012.01.04 | News

ANALYSIS: STORAGE START-UPs IN 2010

52 investment rounds vs. 49 in 2008 and 2009

by Jean Jacques Maleval | 2011.01.03 | News

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter