Yangtze Memory Technologies Company Leads Chinese NAND Flash Market

According to TrendForce

This is a Press Release edited by StorageNewsletter.com on December 26, 2017 at 2:32 pmTrendForce Corp.‘s report, Breakdown Analysis of China’s Semiconductor Industry, outlines the landscape of China’s dynamic and fast-growing semiconductor industry, and reveals that the memory segment will be a focus for the industry, considering that China now heavily relies on imported semiconductor components, and that semiconductor is a sensitive sector which may have potential applications in national security.

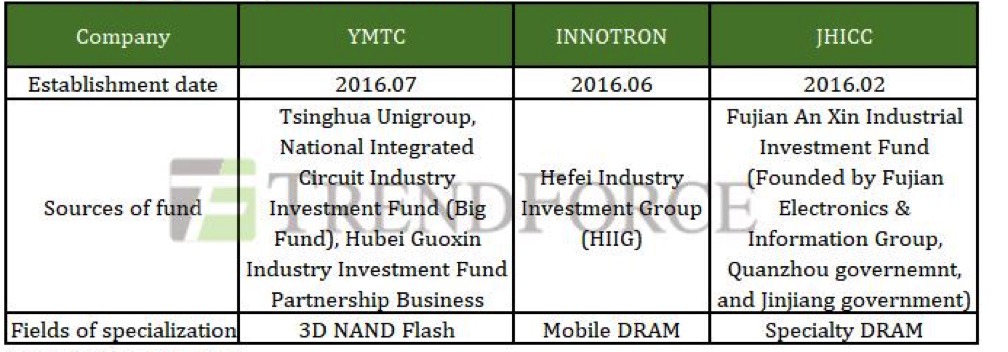

Backed by large sum of funds and government-initiated resources, China has embarked on the development of memory segment, where three major domestic players have emerged, including Fujian Jin Hua Integrated Circuit (JHICC), Innotron Memory, and Tsinghua Unigroup.

Attempts to acquire technologies from foreign companies met resistance in early stages of the development, including Tsinghua Unigroup’s attempt to make technical cooperation deals with Micron, and China-backed funds’ proposals to acquire U.S.-based chipmakers. But China continues to aggressively headhunt for industry talents worldwide, for instance, from Taiwan, Japan, and Korea. The strategy has changed from seeking intellectual property authorization to domestic R&D, showing the strong determination of China to develop its domestic memory fabrication.

JHICC and Innotron respectively focus

on specialty DRAM and mobile DRAM

In the DRAM sector, China has adjusted its strategy to reallocate the originally-scattered resources guided by a more explicit goal. From the technical perspective, Chinese memory suppliers have been laying the foundation for all DRAM segments except graphic DRAM.

JHICC and Innotron are currently two leading DRAM manufacturers in China. JHICC mainly focuses on specialty DRAM R&D and targets at the market of consumer electronics. Backed by large domestic consumption, JHICC is expected to expand its production capacity. Assisted by government subsidies, JHICC may even affect their business strategies in China, and obtain patents to enter the international market at the end of 2018, at the earliest.

While JHICC avoids competing with major foreign memory suppliers in mainstream applications, Innotron has been focusing on mobile DRAM, a key product of major foreign memory makers. Mobile DRAM currently accounts for the highest percentage in all memory products, but has high technical barriers for fabrication since it has strict requirements of reducing power consumption. However, given that Chinese brands have accounted for over 40% of global smartphone shipments, if LPDDR4 enters mass production successfully, together with subsidies and supportive policies, Chinese government may partially achieve its goal of lowering its reliance on imported memory products.

Yangtze Memory Technologies Company (YMTC) takes lead in NAND flash market,

with early development focusing on low-end products

As for NAND flash sector, YMTC, a subsidiary of Tsinghua Unigroup, has taken the lead among Chinese domestic semiconductor enterprises. It focuses on the domestic market in the early stage of development, and will first develop low-end products such as memory cards and USB drives because its technology is still not competitive with other established global suppliers. It will not enter the SSD market until its technology advances to 64/96-layer. However, SSD market is highly competitive, so it is not easy for YMTC to gain cost competitiveness without the support from government. Therefore, taking advantages of Chinese large domestic market will be the feasible strategy for Tsinghua Unigroup to achieve growth.

Furthermore, after YMTC was founded, XMC shifts its focus to NOR flash production. Although the trial manufacturing line of NAND flash is currently set in XMC, the production of NOR flash and NAND flash will be spilt to the two companies, after YMTC finishes the construction of new site in Wuhan Donghu New Technology Development Zone.

TrendForce points out that the next 3 to 5 years will be a crucial period for China to find out whether its strategy of developing memory fabrication works. Deployment in IP will be particularly significant. In order to negotiate and compete with established global chipmakers, Chinese government and semiconductor manufacturers will need to take advantage of its domestic market, and meanwhile, constantly enhance their product development ability and production capacity.

Emerging memory manufacturers in China

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter