NAND Flash Brand Supplier Revenue Falls 4.5% From 3Q13 to 4Q13 – DRAMeXchange

Top 3 being Samsung, Toshiba and Micron

This is a Press Release edited by StorageNewsletter.com on March 6, 2014 at 3:12 pmAccording to DRAMeXchange, a division of research firm TrendForce Corp., in addition to NAND flash capacity adjustments due to the fire at SK Hynix, NAND flash vendors were overly optimistic towards OEM demand in the fourth quarter, resulting in supply that exceeded demand for the quarter.

As such, NAND flash brand suppliers’ revenue fell to $6.168 billion in the fourth quarter of 2013, a 4.5% drop from the previous quarter, but a 16% increase over the same period in 2012. As advanced technology improves yield rates, the NAND flash industry will continue to experience steady growth.

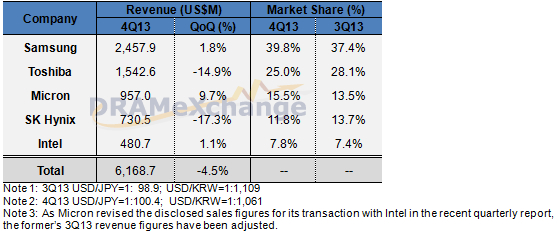

Looking at the NAND flash brand supplier revenue ranking for the fourth quarter of 2013, Samsung maintained its lead with $2.457 billion for a slight increase in market share to 39.8%. Toshiba came in second earning $1.542 billion, market share falling to 25%. Micron ranked third with $957 million in sales, while SK Hynix’s revenue dropped to $730 million after reallocating NAND flash capacity to DRAM in the wake of the fire. The Korean supplier’s market share was 11.8%. Intel’s revenue was $487 million, taking 7.8% of the market.

4Q13 Sales Ranking of Branded NAND Flash Makers

(Source, DRAMeXchange, February 2014)

Samsung

As disappointing sales of Samsung’s high-end smartphones negatively impacted mobile NAND products, the supplier’s fourth quarter NAND flash revenue only grew 1.8% compared to the previous quarter. ASP fell by nearly 10% in the fourth quarter, while quarterly bit shipment volume only increased by 5%. As for technology migration, Samsung’s eMMC, eMCP, and SSD are advancing to the 19nm process, while 3-bit MLC embedded applications have made it into the supply chains of several major PC and smartphone manufacturers. Advanced 1znm products are slated to begin volume production in the second quarter, while 3D NAND enterprise SSD samples were sent to cloud computing suppliers for testing in the fourth quarter. Samsung’s new fab in Xian, beginning operations this quarter, will serve as the base for 3D NAND flash production. As cloud computing stimulates enterprise SSD demand growth, in 2014 Samsung plans to switch its strategic focus from eMMC to enterprise SSD.

Toshiba

Toshiba’s NAND flash revenue fell to $1.542 billion in the fourth quarter, a nearly 15% QoQ decrease, mainly due to disappointing client shipments. Additionally, market oversupply in the fourth quarter resulted in a greater decline than expected in ASP, causing the noticeable shrink in revenue. As for Toshiba’s technology, the supplier successfully migrated from the 19nm process to the A-19nm process in the fourth quarter, and yield rate improvements should begin to take effect this quarter. Volume production of A-19nm embedded products will begin in the second quarter, hopefully stimulating revenue growth. Additionally, to avoid the risk of having too many clients concentrated in the same sectors, Toshiba is actively seeking notebook and mobile device OEM orders.

SK Hynix

According to SK Hynix’s fourth quarter earnings report, after reallocating capacity in September due to the fire at the supplier’s Wuxi fab, fourth quarter NAND flash revenue amounted to $730 million, a 17% QoQ decrease. Bit shipment volume also fell, by 14% QoQ. SK Hynix’s ASP for the fourth quarter also dropped 5% QoQ, as the ratio of high-density eMMC sales continues to climb. TrendForce expects SK Hynix will gradually reallocate capacity that was transferred to DRAM in the aftermath of the fire back to NAND flash production beginning in the first quarter, with a goal of returning to pre-fire levels before the second half of the year. In terms of technology, SK Hynix has already sent 16nm eMCP and eMMC samples to clients and expects to begin volume production in the second quarter. The supplier is also accelerating development of its NAND flash controller chips to make its eMMC and SSD products more competitive.

Micron

Micron’s NAND flash revenue increased by 9.7% QoQ to $957 million. As its Singapore fab successfully transitioned from DRAM to NAND production, bit shipment volume increased by 17% QoQ. ASP dropped by 6% QoQ, but unit cost also fell by 7% QoQ due to a higher ratio of 20nm eMMC and SSD sales, helping Micron maintain profitability. Looking at the supplier’s strategy, SSD products have become the focus of Micron’s operations, accounting for 48% of total NAND flash revenue. Volume production of 16nm products is scheduled to begin next quarter, and 3D NAND flash samples may be shipped as early as next quarter, with volume production to follow in the second half of 2015. With the addition of Elpida to the Micron group, the supplier is gradually becoming more competitive in the mobile NAND flash sector.

Intel

Although enterprise SSD demand remains strong, the competition is also heating up as Samsung and other leading vendors focus their efforts on the sector. As such, Intel’s fourth quarter NAND flash revenue only increased by 1.1% QoQ, arriving at $480 million. However, since Intel currently has the largest enterprise SSD market share and its product portfolio consists mostly of high-end products, the supplier is rapidly advancing all SSD production to the 20nm process to lower costs and increase its competitive advantage.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter