Spot Market for DRAM Struggles in 1H24

Price challenges loom in 2H24.

This is a Press Release edited by StorageNewsletter.com on September 5, 2024 at 2:02 pmThis market report, published on August 29, 2024, was written by TrendForce Corp.

Spot Market for Memory Struggles in First Half of 2024

Price Challenges Loom in Second Half

Memory module makers have been aggressively increasing their DRAM inventories since 3Q23, with inventory levels rising to 11–17 weeks by 2Q24. However, demand for consumer electronics has not rebounded as expected. For instance, smartphone inventories in China have reached excessive levels, and notebook purchases have been delayed as consumers await new AI-powered PCs, leading to continued market contraction.

This has led to a weakening in spot prices for memory products primarily used in consumer electronics, with 2Q24 prices dropping over 30% compared to 1Q24. Although spot prices remained disconnected from contract prices through August, this divergence may signal potential future trends for contract pricing.

In 2Q24, module makers saw a significant 40% Y/Y decline in shipments through retail channels for consumer NAND flash, reflecting severe challenges in the global consumer market for memory. While the memory industry is typically subject to cyclical fluctuations, the sharp decline in shipments during 1H24 exceeded market expectations, indicating that demand is unlikely to recover substantially in 2H24.

Factors such as inflation and rising interest rates have impacted consumer spending and indirectly dragged down shipments of consumer memory modules. Additionally, the ongoing increase in NAND flash wafer prices has further strained the operating costs of module makers. Prices must remain attractive to stimulate demand as consumers become more cautious with their spending, limiting the ability of module makers to pass on increased costs, thereby compressing profit margins.

It remains unclear whether AI smartphones or AI PCs will have significant applications in the coming quarter. Even if adoption rates improve due to the promotion of platforms, a widespread upgrade cycle is unlikely, and as such DRAM prices may not see substantial support.

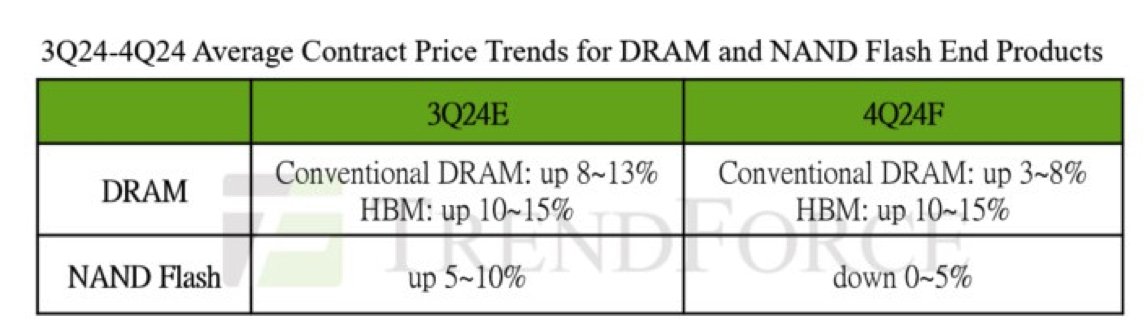

Looking ahead to 2025, although DRAM prices are expected to rise gradually each quarter, this increase will be driven primarily by the growing penetration of HBM3e – raising average prices – as well as constrained supply due to limited new capacity. The anticipated increase in DRAM prices could fall short of expectations if consumer demand remains weak.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter