Organizations Spent $7.6 Billion on Compute and Storage Hardware Infrastructure

To support this workload in 2H22

This is a Press Release edited by StorageNewsletter.com on May 12, 2023 at 2:02 pmStructured Databases/Data Management continued driving the largest share of enterprise IT infrastructure spending in 2H22, according to IDC Worldwide Semiannual Enterprise Infrastructure Tracker: Workloads.

Organizations spent $7.6 billion on compute and storage hardware infrastructure to support this workload in 2H22, which represents 9.1% of the market total.

Y/Y growth was relatively low compared to other workloads with a 6.5% increase in value compared to 2H21.

Unstructured Database and HR/Human Capital Management (HCM) saw the highest Y/Y growth in hardware infrastructure demand with spending growing at 36.7% and 35.4% respectively from 2H21.

However, these are also the 2nd and 4th smallest workloads regarding consumption of compute and storage infrastructure, respectively, with Unstructured Database accounting for $2.4 billion in spending, while HCM accounting for $2.7 billion in spending.

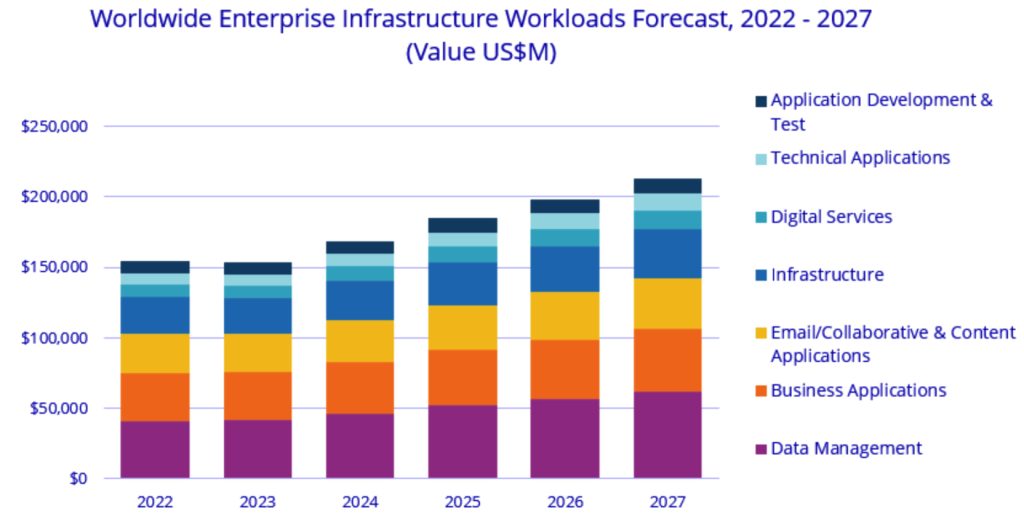

IDC estimates spending on compute and storage systems across 19 mutually exclusive workloads, defined as applications and their datasets. The full taxonomy including definitions of the workloads can be found in IDC’s Worldwide Semiannual Enterprise Infrastructure Tracker: Workloads Taxonomy, 2021 (IDC #US48332521). The majority of workloads map to secondary or functional software markets while several, including Content Delivery and Digital Services, have no equivalent in the software market structure. Workloads are further consolidated into 7 workload categories, which include application development and testing, business applications, data management, digital Services, email/collaborative and content applications, infrastructure, and technical applications.

In 2022, the Data Management workload category, which includes 5 workloads – AI lifecycle, business intelligence and analytics, structured database/data management, text and media analytics, and unstructured database – was the largest workload category with $41.4 billion in spending on compute and storage infrastructure products. It will remain the largest throughout the forecast period with a 5-year CAGR of 8.3% and reaching $61.7 billion in infrastructure spending in 2027. Most of the growth in this category will come from the fastest growing workloads related to unstructured data and artificial intelligence, all of which will grow at a double-digit CAGR.

Data Management will also be the largest category of infrastructure spending in both shared and dedicated cloud environments at 14.1% CAGR and $26.6 billion spending in 2027 in shared, 4.9% CAGR and $35.2 billion in 2027 in dedicated environments (this includes dedicated cloud and non-cloud infrastructure deployments). Technical Applications will be the fastest growing workload category for compute and storage infrastructure consumption in both shared environments at 15.7% CAGR, and in dedicated environments at 5.8% CAGR. Cumulative spending on infrastructure for the Technical workload category will reach $12.0 billion in 2027.

As enterprise workloads continue to move into public cloud, investments in shared infrastructure (a hardware base for delivering public cloud services) will be increasing faster than investments in dedicated infrastructure across all workloads. Similarly, the growth in investments compute and storage systems for cloud-native workloads will be 2x as high as the growth in spend on infrastructure supporting traditional workloads (11.6% vs 5% CAGR) although traditional workloads will continue accounting for majority of spend during the forecast period (71.4% in 2027).

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter