Total 2Q22 Enterprise SSD Revenue to Grow 31% Q/Q at $7.32 Billion

Thanks to server shipment growth and spiking pricing

This is a Press Release edited by StorageNewsletter.com on September 5, 2022 at 2:02 pmAccording to TrendForce Corp.‘s research, material supply improvement and spiking demand for enterprise SSDs from North American hyperscale data center and enterprise clients in 2Q22 coupled with the Kioxia contamination incident in 1Q22 prompted customers to ramp up procurement to avoid future supply shortages.

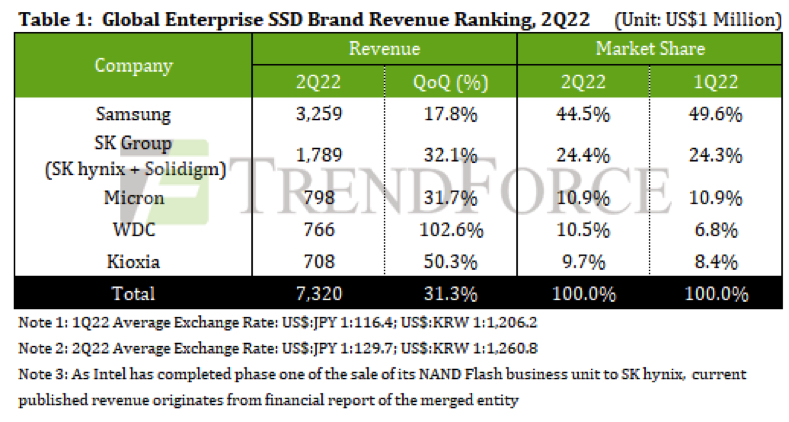

Manufacturers also give priority to meeting the needs of server customers due to the high pricing of enterprise SSD. In 2Q22, overall revenue of the enterprise SSD market increased by 31.3% to $7.32 billion.

As the market leader, Samsung has grown its enterprise SSD revenue to $3.26 billion with the recovery of enterprise SSD procurement. Especially in the second quarter, when orders for other consumer products continued to decline, enterprise SSD became the company’s outlet for reducing production capacity. At present, Samsung has been continuously investing in the development of next-gen transmission spec products such as the CXL 2.0 product released at FMS in early August, in order to maintain a leading position in the market. It is worth noting that the successor product to Samsung’s current 128-layer enterprise SSD is 236-layer but the mass production schedule of this process may fall in 2H23.

SK Hynix and Solidigm will launch 176-layer enterprise SSD early next year.

In addition Micron has already mass-produced 176 layers while Samsung seems to be feeling cost pressure, especially since YMTC has just released a PCIe 4.0 enterprise SSD.

In view of this, Samsung plans to launch 176-layer products in China next year to compete with other manufacturers. Under China’s localization policy and the competition from high-level SSDs launched by other manufacturers, Samsung’s enterprise SSD market share in China is bound to be challenged.

In 2Q22, Solidigm finally divested itself of master controller IC supply and posted significant growth, while SK hynix continued to expand its partnership with North American customers to grow PCIe SSD shipments. The company’s 128-layer product has gradually become a focus of supply, driving SK Group’s enterprise SSD revenue growth by 32.1%, reaching $1.79 billion. SK Group’s SSD business strategy is crystalizing and the company will mass-produce 176-layer TLC solutions next year. In terms of QLC, Solidigm will introduce a 192-layer process and is even planning PLC (Penta Level Cell) products. TrendForce indicates, as SK Group plans various products at different price points to meet all the storage needs of server customers, the company will have an opportunity to expand its market share and narrow the gap with leading manufacturers in the future.

Micron’s revenue in 2Q22 rose 31.7% Q/Q to $798 million, ranking ≠3. Although the company’s 176-layer PCIe 4.0 products have yet to ramp up, its leading NAND flash process and cost advantages over other manufacturers have attracted more companies willing to verify company’s PCIe 4.0 products. The firm continues to increase its enterprise SSD shipments to ensure that future revenue growth momentum will not decline due to weak consumer products.

Ranked ≠4, WDC’s 2Q22 enterprise SSD revenue was $766 million, doubling from the previous quarter, mainly due to the impact of the raw material pollution incident in the first quarter. Customers have replenished inventory ahead of time to avoid the uncertainty of supply shortages while WDC has given priority to server customers in order to increase profit margins and thereby drive revenue. The company still hopes to improve the competitive strength of enterprise SSD products but, due to a lack of R&D manpower, the firm’s focus will gradually shift to North American customers and its support of the Chinese market will gradually weaken, mainly because the verification process for North American hyperscale data center customers is relatively long and verification standards complicated. In order to clearly ensure the increase of market share in the future, North America is preferred as the primary sales focus to enhance the competitive strength of WDC enterprise SSD.

In addition to rebounding purchase orders in 2Q22, its contamination incident also compelled some enterprise customers to purchase products in advance, driving Kioxia’s revenue up to $708 million, ranking ≠5.

In addition to continuously increasing its proportion of PCIe 4.0 shipments, Kioxia also accelerated the launch of more enterprise SSD products. In addition to mass production of PCIe 5.0 products in 2H22, the company also launched a new gen of SAS 3.0 solutions. With company’s apparent focus on the development of enterprise market products and the availability of PCIe 5.0 products, the firm is estimated to have an opportunity to expand its market share of enterprise SSD products next year.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter