Total DRAM Revenue Falls 4.0% Q/Q in 1Q22 Reaching $24 Billion

As inflation intensifies and consumer demand weakens.

This is a Press Release edited by StorageNewsletter.com on May 24, 2022 at 2:02 pm![]() This market report, published on May 18, 2022, was written by Ken Kuo, senior research VP, TrendForce, Inc.

This market report, published on May 18, 2022, was written by Ken Kuo, senior research VP, TrendForce, Inc.

Global DRAM Revenue Falls 4.0% Q/Q in 1Q22

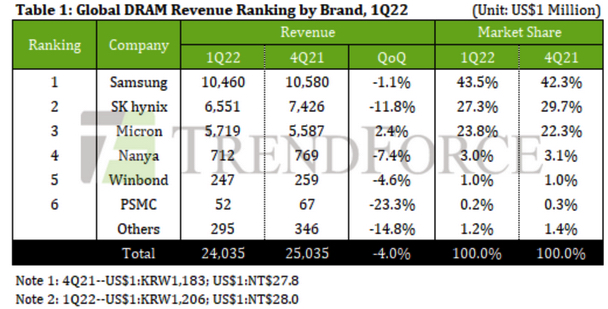

According to TrendForce investigations, total DRAM revenue in 1Q22 decreased by 4.0% Q/Q, reaching $24.03 billion.

The primary reason for this drop stems from market inflation, weakening demand, and the outbreak of the Russian-Ukrainian war at the end of February affecting the performance of terminal consumption. At the same time, client-end inventory levels continue to rise, so their primary goal has become digesting inventory. Due to sluggish overall sales momentum, the prices of various DRAM products fell, resulting in overall DRAM revenue in 1Q22 succumbing to decline.

Thanks to favorable demand in the PC and automotive market, the revenue of Micron, one of the 3 major DRAM manufacturers, rose slightly by 2.4%. But Samsung and SK hynix revenue fell by 1.1% and 11.8% respectively. In total, these 2 South Korean manufacturers account for a market share of 70.8%, remaining firmly in the top 2.

Affected by falling contract pricing, the operating profit ratios of these 3 companies were revised downward, with Samsung, SK hynix, and Micron dropping to 48%, 39%, and 40.1%, respectively. Looking forward to subsequent developments, as DRAM continues to move to advanced processes, cost is expected to be further optimized. If negative market factors no longer accumulate, profits for these companies are expected to improve further.

In terms of production capacity planning, Samsung’s 2022 goal remains focused on capacity expansion. DRAM wafer starts at its new P3L fab is expected in mid-2023 at the earliest and, in terms of products, the company will continue pushing towards DDR5. In 2H22, the DDR5 proportion of production dedicated to PCs and servers is expected to increase. SK hynix’s M16 fab in Korea and Wuxi fab in China have also exhibited a slight increase in wafer starts. However, since the migration of M14 to logic products caused a drop in DRAM wafer starts, total wafer starts only increased slightly.

In terms of technology, SK hynix has already allocated a small amount wafer starts in the 1alpha nm process and expects to achieve a certain economy of scale by the end of the year.

Micron has no expansion in overall wafer starts this year, and capacity contribution from its A3 fab in Taiwan will likely fall in 2024 at the earliest. It also introduced the 1alpha nm process in 2H21 and wafer starts for the 1beta nm process is possible in 1H23, the fastest progress among the big three DRAM manufacturers.

In terms of Taiwanese manufacturers, Nanya is still focusing on the production of consumer DRAM but, with PC DRAM prices on the decline, overall revenue decreased by 7.4%. Mass production is expected for the 1Anm process by the end of the year but expansion of overall scale will depend on the completion of the company’s new Fab5A in 2025.

PSMC’s revenue calculation primarily references standard DRAM products produced in-house and does not include its DRAM foundry business. Revenue in 1Q22 fell by approximately 23%, mainly due to a decrease in the demand for company’s own products from major clients. However, if foundry revenue is included, revenue will grow by 3%, bucking trends.

Winbond’s revenue declined slightly by 4.6%, due to its product mix. Part of its production capacity was migrated to NOR flash memory, resulting in a recent decrease in DRAM wafer starts. However, since equipment installation will begin at the company’s Kaohsiung Lujhu fab this year, new production capacity is expected to become available gradually in 2H22.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter