WW Integrated Infrastructure and Platforms Revenue Increases 38.5% Y/Y in 1Q14 at $1.9 Billion – IDC

1/ Cisco/NetApp, 2/ VCE, 3/ EMC for infrastructure

This is a Press Release edited by StorageNewsletter.com on June 27, 2014 at 2:54 pmAccording to the International Data Corporation‘s Worldwide Quarterly Integrated Infrastructure and Platforms Tracker, the worldwide integrated infrastructure and platforms market increased revenue 38.5% year over year to $1.95 billion during 1Q14.

The market generated 653.8PB of new storage capacity shipments during the quarter, which was up 72.3% compared to the same period a year ago.

“As the market moves to the 3rd Platform, IT customers are seeking to leverage cloud, social, mobile, and big data in their businesses. Transforming an IT environment requires a new approach to systems,” said Jed Scaramella, research director, enterprise servers. “Many customers see the convergence of server, storage, and networking in Integrated Systems as a means to deliver IT efficiency and agility. IDC expects to see more workload-optimized systems come to market in the near term.“

“Once again we witnessed an increasing number of organizations around the world leveraging integrated systems to address longstanding datacenter infrastructure inefficiencies,” said Eric Sheppard, research director, storage. “As such, this market remains one of the fastest growing segments of the overall infrastructure market.“

Integrated Platforms vs. Integrated Infrastructure

IDC distinguishes between two market segments: Integrated Platforms and Integrated Infrastructure. Integrated Platforms are integrated systems that are sold with additional pre-integrated packaged software and customized system engineering optimized to enable such functions as application development software, databases, testing, and integration tools. Integrated Infrastructure systems are designed for general purpose, distributed workloads that are likely to have differing performance profiles. While integrated infrastructure is similar to integrated platforms in that it will leverage the same infrastructure building blocks, it is not optimized for a specific workload.

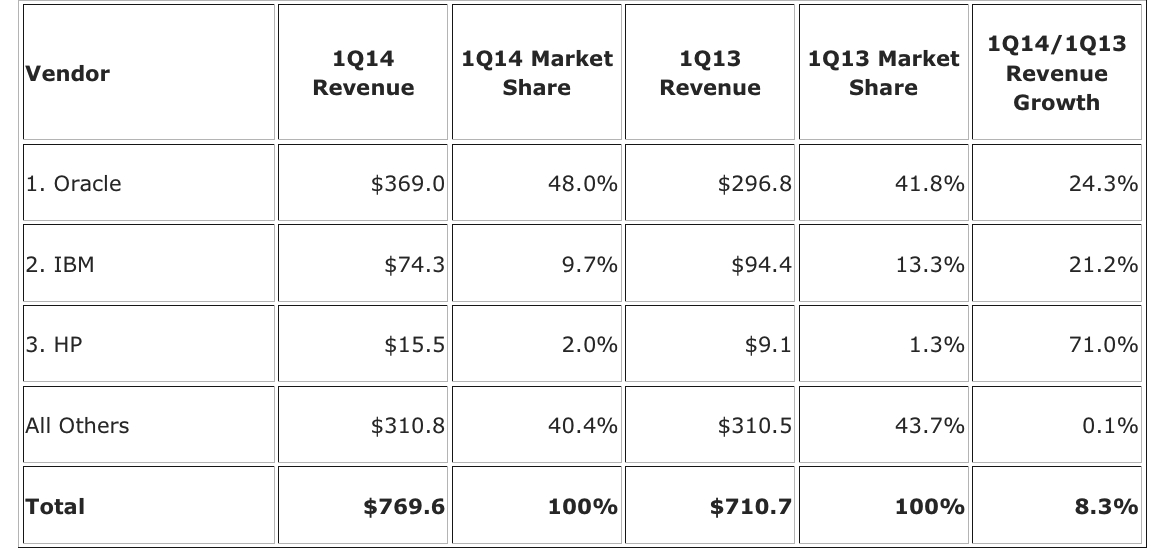

During the first quarter of 2014, the Integrated Platforms market generated revenues of $769.6 million, which represented an 8.3% year-over-year growth rate and 39.5% of the total market value. Oracle was the largest supplier of Integrated Platform systems with $369.0 million in sales, or 48.0% share of the market segment.

Top 3 Vendors, WW Integrated Platforms, Q1 2014

(revenue in $ million)

(Source: IDC Worldwide Integrated Infrastructure & Platforms Tracker, June 26, 2014)

Correction: 1Q14/1Q13 revenue growth for IBM is not 21.2% but -21.2%

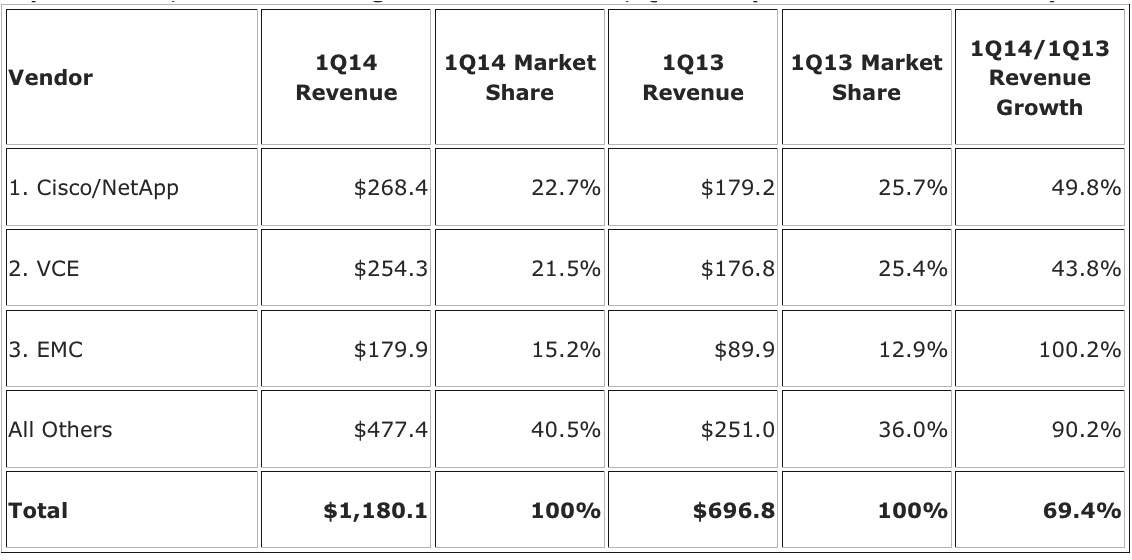

Integrated Infrastructure sales grew 69.4% year over year during the first quarter of 2014, generating nearly $1.2 billion worth of sales. This amounted to 60.5% of the total market value. FlexPod by Cisco/NetApp was the top-ranked supplier of Integrated Infrastructure in the quarter, generating revenues of $268.4 million and capturing a 22.7% share of the market segment.

Top 3 Vendors, WW Integrated Infrastructure, Q1 2014

(revenue in $ million)

(Source: IDC Worldwide Integrated Infrastructure & Platforms Tracker, June 26, 2014)

Taxonomy Notes:

IDC defines integrated infrastructure and platforms as pre-integrated, vendor-certified systems containing server hardware, disk storage systems, networking equipment, and basic element/systems management software. Systems not sold with all four of these components are not counted within this tracker. Specific to management software, IDC includes embedded or integrated management and control software optimized for the auto discovery, provisioning, and pooling of physical and virtual compute, storage, and networking resources shipped as part of the core, standard integrated system.

Subscribe to our free daily newsletter

Subscribe to our free daily newsletter